Changes to the Consumer Protection Act and Stricter Creditworthiness Assessment Requirements

Changes to the Consumer Protection Act and Stricter Creditworthiness Assessment Requirements

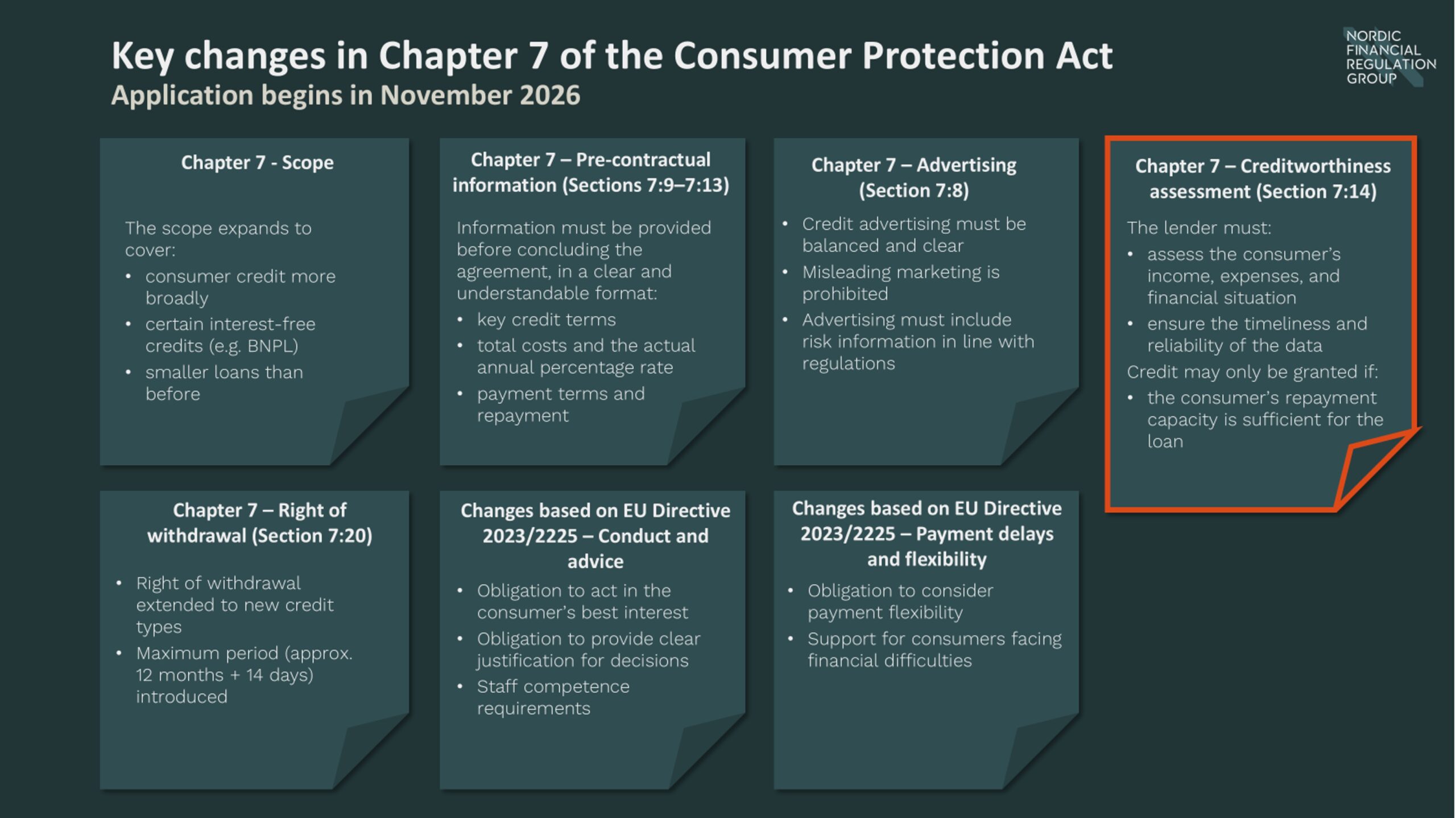

Directive (EU) 2023/2225 has introduced a comprehensive reform of EU consumer credit regulation, expanding its scope to include BNPL (Buy Now, Pay Later) models, small loans, and short-term credit, while tightening requirements related to disclosure, marketing, and creditworthiness assessments. In Finland, this has led to a broad reform of the Consumer Protection Act during 2025–2026, increased registration obligations, and stricter regulation particularly concerning small loans and e-commerce payment methods. Key changes related to creditworthiness assessment will enter into force on 20 November 2026, alongside other significant reforms.

Key Changes to the Consumer Protection Act

Expanded registration requirements

According to a supervisory bulletin issued on 23 January 2026 by Finnish Financial Supervisory Authority, new consumer credit providers and intermediaries will come under its supervision. At the same time, the obligation to register as a credit provider will be extended to include certain entities already supervised by the authority that grant consumer credit. Operators intending to continue granting or intermediating consumer credit under Chapter 7 of the Consumer Protection Act after the legislative changes take effect on 20 November 2026 must register in the authority’s register. The authority has accepted registration notifications from credit intermediaries since 20 March 2026 from entities falling within the scope of the new Act on certain consumer credit intermediaries. Applications submitted by 20 May 2026 will be processed before the legislative changes enter into force.

Emphasis on creditworthiness assessment

Creditworthiness assessment is a key obligation in granting consumer credit, and its importance will further increase under the new regulation. The creditor must carry out a careful assessment based on up-to-date and sufficient information regarding the consumer’s ability to repay the credit.

Key findings:

- The positive credit register is used, but its use varies (especially insufficient consideration of existing loans)

- The accuracy of customers’ financial information is not always sufficiently verified

- Affordability assessments do not always consider all relevant expenses or future changes (e.g. interest rates, income stability)

- Documentation deficiencies exist (e.g. retention periods too short)

- Not all actors have assessed their credit decision models from a non-discrimination perspective

The authority requires institutions to correct identified deficiencies and will use the findings to guide future supervision.

In January 2026, the authority published its inspection and thematic review plan, which includes a new review of creditworthiness assessments in 2026 (covering EEA credit institutions and consumer credit providers).

Requirements for creditworthiness assessment

Under the revised Consumer Protection Act, before concluding a credit agreement, the creditor must carefully assess the consumer’s creditworthiness using necessary information about their income, expenses, and financial situation.

Key requirements:

-

Sufficient and reliable information base

- The assessment must be based on up-to-date and verified information

- Information must be obtained from the consumer and key data sources, such as the positive credit register

- Accuracy of information must be appropriately verified

- In certain limited cases (e.g. completely interest-free and cost-free credit), the use of data sources may be more limited, but the assessment must still be sufficient

-

Individual affordability assessment

The assessment must consider:

- Income and its stability

- Actual expenses (e.g. housing costs)

- Existing debts and obligations

- Assets and guarantee liabilities

The assessment must reflect the consumer’s actual repayment capacity and must not be based solely on collateral or statistical assumptions.

-

Positive credit register

The positive credit register is a key data source and, as a rule, an essential part of creditworthiness assessment.

-

Documentation requirement

The creditor must document:

- Data used

- Assessment methods

- Conclusions reached

Documentation must be sufficiently comprehensive and clear so that an authority can review it without additional clarification. All data must be specified, calculations transparent and reproducible, and decisions justified and assessable afterwards.

Automated decision-making and transparency

If decisions are made automatically, the creditor must ensure transparency and understandability of the process.

Purely automated decision-making without appropriate safeguards is not permitted. The General Data Protection Regulation requires that the consumer has the right to:

- Be informed about automated decision-making

- Request a clear explanation of the decision

- Present their own view

- Request a human review of the decision

The Consumer Credit Directive complements and specifies GDPR in the context of creditworthiness assessment by:

- Emphasizing transparency in credit decisions

- Requiring that the consumer is informed about the assessment

- Strengthening the right to justification and understandable explanation

Practical implementation

Step 1: Data collection

- Verification of applicant’s income (salary and benefits)

- Comprehensive mapping of expenses

- Existing debts and financial commitments

- Data from key registers

Step 2: Analysis and credit models

- Calculation of actual disposable income

- Assessment of repayment capacity

- Sensitivity analysis (e.g. rising interest rates, income changes)

Step 3: Decision principle

Credit may only be granted if it is likely, based on the assessment, that the applicant can meet repayment obligations without significantly reducing their standard of living throughout the credit period.

The assessment should not rely on assumptions such as:

- Significant future reduction in consumption

- Refinancing the loan to enable repayment

Step 4: Documentation and controls

Documentation must be:

- Transparent and reproducible

- Assessable afterwards

- Reviewable by authorities without additional clarification

Consequences of inadequate assessment

An inadequate creditworthiness assessment may lead to significant legal consequences. In certain situations, the creditor may lose the right to charge interest or other credit costs, partially or entirely. The application of sanctions depends on the nature of the breach and case-by-case evaluation.

NFR’s supervisory experience supporting creditworthiness processes

Experts at NFR Group assess whether a company’s creditworthiness assessment process meets applicable regulatory requirements, particularly those under Chapter 7 of the Consumer Protection Act (consumer credit) and the Consumer Credit Directive (CCD2). They also support the design, development, and implementation of processes where necessary. The assessment covers procedures, controls, and documentation related to creditworthiness evaluation (especially Section 14 of Chapter 7).

The review also examines terms and contractual documentation of existing credit arrangements and identifies potential update needs ahead of legislative changes entering into force on 20 November 2026 (national implementation of CCD2). At the same time, it ensures that governance documents, policies, and internal control arrangements are consistent and support compliant operations.

The review may also extend to marketing and sales channels to ensure compliance with consumer credit requirements (e.g. Chapter 7 Sections 8–13 of the Consumer Protection Act) and promote responsible lending practices. Additionally, procedures related to partners and third parties—especially credit intermediaries—are assessed considering applicable regulations.

Through this collaboration, companies receive a comprehensive assessment of the compliance and development needs of their creditworthiness and risk assessment models. The work helps prepare for regulatory changes, improves transparency and efficiency, and leverages NFR’s practical supervisory expertise.

Are your creditworthiness assessment processes ready for the 2026 regulatory changes? Contact us to ensure compliance.

AML package

AML package

The AML package was adopted by the Council of the European Union in May 2024 and aims to harmonize the anti-money laundering legislation within the EU. The AML package mainly consists of three parts:

AMLR

Regulates the requirements for business operators, such as banks and accounting consultants. The AMLR will enter into force immediately in all Member States and replace current national legislation from 10 July 2027.

AMLD 6

Specifies how national competent authorities should be organized and should be implemented through national legislation.

AMLA-R

Regulates the new European Anti-Money Laundering and Counter-Terrorism Financing Authority (AMLA)

What do we know and what remains?

What do we know and what remains?

The scope and content of the AMLR have been established and will apply from 10th of July 2027. However, the AMLR will be supplemented by approximately 20 Regulatory Technical Standards (RTS), Guidelines (GL) and Implementing Technical Standards (ITS), which will specify the requirements further in areas such as KYC, internal procedures and outsourcing. AMLA has presented a plan for the development of these, where several drafts will be published in 2026. AMLD6, which regulates, among other things, the work of the Financial Supervisory Authorities and the Financial Intelligence Units as well as the central register of beneficial owners, is to be transposed into national law. The more detailed formulation of this is ongoing and remains to be followed.

Even after July 2027, further additions will be introduced. These include requiring football clubs to apply the AMLR from 10th of July 2029, and from the same date, the introduction of lower thresholds for determining beneficial ownership may be applied to selected categories of companies.

A selection of upcoming RTS, ITS and GL from AMLA

Q1 2026

- Customer due diligence (28.1)

- Identification of business relationships and occasional or linked transactions (19.9)

Q2 2026

- Minimum requirements for group-wide policies, including among other things information exchange (16.4)

Q3 2026

- Minimum requirements for the content of the general risk assessment (10.4)

- Risks to consider when entering into a business relationship (20.3)

- Ongoing monitoring of business relationships and transactions (26.5)

Q1 2027

- Scope of internal policies, including internal roles (9.4)

- Q1 2026Customer due diligence (28.1)

Identification of business relationships and occasional or linked transactions (19.9)

- Q2 2026

Minimum requirements for group-wide policies, including among other things information exchange (16.4)

- Q3 2026

Minimum requirements for the content of the general risk assessment (10.4)

Risks to consider when entering into a business relationship (20.3)

Ongoing monitoring of business relationships and transactions (26.5)

- Q1 2027

Scope of internal policies, including internal roles (9.4)

What does this mean for you as an obliged entity

What does this mean for you as an obliged entity

Since AMLR is part of the AML package that regulates the requirements for operators, it is primarily this part of the AML package that is relevant if you are an obliged entity. However, it is important to understand that both AMLD6 and AMLA-R can have a direct and indirect impact on your business. AMLA-R contains, for example, requirements for how supervisory authorities should assess the risk of operators, which has been clarified via an RTS in the area. Further AMLD6 regulates areas such as access to the central register of beneficial owners and collaboration with authorities.

In dialogue with our customers, we see that the parts of AMLR perceived as most challenging vary. What type of operator you are, how you are organized and the size of your business are examples of factors that affect challenges in regulatory adaptation. Other factors that can also have an impact are whether you are part of a group, the proportion of outsourced operations, the number of employees and existing access to data. Some of the areas that are most discussed with our customers today include:

- Outsourcing – AMLR introduces restrictions on which parts of the AML work are allowed to be outsourced, the restrictions also apply to intra-group outsourcing. This means that AMLR may entail a need for a change in responsibilities and organization.

- Roles – The current roles within the AML legislation will disappear and be replaced by two new roles, Compliance Manager and Compliance Officer. Where the Compliance Officer should be placed, in the first or second line, is the source of many discussions. Depending on where the function is located, reorganization and reallocation of responsibilities may be required.

- Group – AMLR directs an increased focus on groups compared to previous regulations. The changes concern both intra-group information sharing, and in cases where a subsidiary that is under the scope of AMLR can «affect» a parent company. The implication is thus that the parent company may also fall within the scope of the AMLR.

- Customer due diligence – AMLR and the published draft RTSs emphasize a risk-based approach and clarify, among other things, what information may be required to meet requirements for purpose and intended nature (previous purpose and nature). New areas that are being added are e.g. place of birth and the destination of the means.

- Beneficial owner – The AMLR specifies the methodology to use to identify the beneficial owner. New requirements for reporting in the event of identified deviations from the central register for beneficial owners are also stipulated in AMLR.

- Targeted financial sanctions – The prevention of targeted financial sanctions being circumvented or not implemented becomes an integral part of everything from customer due diligence and general risk assessment to the division of responsibility.

- Expanded reporting requirements – The reporting requirements are now expanded to include certain types of threshold-based reports, which places demands on a new type of monitoring.

- Expanded access to data – Financial sector supervisors will assess risk based on a uniform methodology based on approximately 100-150 data points. These data points are expected to be integrated into periodic reporting to the Financial Supervisory Authority, which is why access to data is important to ensure now.

How NFR Group can support you

How NFR Group can support you

Based on the purpose of the regulations, our advisors, with experience from both supervisory authorities and operational and strategic roles, can support you in succeeding with your implementation project. The scope, focus and structure of our advice are adapted based on your individual needs to create long-term solutions that are compatible with your individual situation. Our advisors have expertise in areas ranging from KYC to risk models and internal governance. Their knowledge base, combined with experience from supervisory dialogues and operational understanding of KYC and TM processes, allows us to support you in most parts of your AMLR journey. Below is a selection of areas where NFR Group can assist with support and expertise.

GAP-analysis

We can help you with a GAP-analysis to identify where your gaps are in relation to the AML package or just a specific part of the package, as well as support you in prioritizing.

Implementation

With our understanding of the operational processes within AML combined with experience from supervisory dialogues, we can help you find appropriate and effective solutions that work in the long run for your organization.

Senior advisor

We can be there as your support and senior advisor during the implementation journey to guide you in regulatory interpretations and priorities throughout the project.

Review of data

Access to data is something that often sounds easier than it is. The AML package will place higher demands on your access to and control of essential data. We have advisors with broad experience of both data analysis and requirements for internal data who can support you in your work to structure and ensure data access.

Training

The AML package will entail changes at a number of different levels of the business. We can help you with training at all levels, from board of directors to investigators.

How will the AML package affect your operations, and what preparations are required ahead of AMLR?

ECB’s Climate Risk Penalties Mark a Turning Point for Banks

ECB’s Climate Risk Penalties Mark a Turning Point for Banks

The European Central Bank’s recent enforcement action against a major European bank has been widely perceived as a landmark moment in the integration of climate‑related and environmental (C&E) risks into prudential supervision. While headlines focus on fine and C&E risks, the underlying story is equally one of data, analytics and methodological rigour. The message to European banks is clear: the era of supervisory tolerance has ended.

C&E Risk Moves from Expectations to Enforcement

In February, the ECB imposed €7.55 million in periodic penalty payments on a large European bank for failing to meet a key supervisory requirement: completing a robust materiality assessment of C&E risks within the mandated timeline. The bank missed its deadline by 75 days, triggering the ECB’s daily penalty mechanism.

This is the ECB’s second climate‑risk‑related penalty in just three months, following a much smaller sanction in late 2025. The escalation sends a clear message: C&E risks non‑compliance is no longer a symbolic issue. It has real financial consequences.

This outcome is a warning shot for major European banks with deep exposure to sectors sensitive to physical climate risks. The financial impact of €7.55 million is manageable for large banks, but the psychological and organisational implications are far more significant and far more costly.

This is no longer about ambition or policy statements — it is about operational delivery.

The Real Issue: Data, Models, and Operationalisation

Although the sanctions stem from climate‑risk shortcomings, the substance of the ECB’s expectations is fundamentally about data and methodology. Banks are being asked to demonstrate that they can:

- Identify material climate exposures through granular, reliable data covering counterparties, assets, and geographies

- Translate climate drivers into quantitative financial risk metrics using transparent, defensible methodologies

- Conduct forward‑looking analysis and stress tests that can be explained and replicated

- Maintain clear data lineage from source to disclosure

The challenge is rarely an unwillingness to recognise C&E risks. Instead, it lies in operationalising C&E risks: consolidating fragmented data, filling gaps with consistent external datasets, and aligning methodologies across risk, finance and business functions. This is where many banks still fall short and where supervisors are now drawing firm lines.

The ECB has been building toward this moment for years. Its 2020 C&E Risk Guide, the 2022 climate stress test, and multiple follow‑up findings have laid out expectations clearly. What has changed is not the guide and the findings, but the willingness to enforce it.

Why the ECB’s Enforcement Matters

The penalties signal a structural shift: climate risk management is evolving from a conceptual requirement to a fully operational component of prudential supervision.

For banks, three implications stand out:

- C&E risks is now a supervisory priority with financial implications.

Non‑compliance affects the bottom line. C&E risks are being treated with the same seriousness as credit or market risk.

- Materiality assessments must be timely, credible and bank‑specific.

High‑level statements are no longer enough. Supervisors expect rigorous data, sector‑level granularity, and documented methodological choices.

- Supervisory escalation is becoming the norm.

Where progress is insufficient, banks should expect intrusive follow‑ups, daily fines, and increased monitoring.

Broader Implications: A New Era of Climate Risk Governance

The ECB’s approach underscores a broader sector‑wide transformation. As regulatory scrutiny intensifies, banks will need to accelerate investment in:

- Integrated C&E risks governance

- Data aggregation and reporting capabilities

- Scenario analysis and stress‑testing frameworks

- Timely remediation of supervisory findings

- Transparent and traceable model governance

C&E risks are no longer an add‑on. It is becoming a core component of risk management and strategic decision‑making.

A Clear Signal for the Banking Sector

The recent penalty imposed by the ECB does more than sanction a delayed materiality assessment. It marks the formal end of the supervisory “grace period” that banks have operated under while developing their C&E risks frameworks. Banks are being told, with growing clarity, that climate risk is financial risk and that managing it requires robust data, credible methodologies and timely execution.

For banks, the lesson is clear: climate risk management can no longer remain a conceptual or qualitative exercise. It must become an operational reality handled at CFO and CRO level or it will come with a price.

Have you aligned risk, finance, and business functions around a consistent and auditable C&E risk methodology?

Ingalill Aspholm

Tel. +358 40 084 0314

Sanctions compliance in finance

Sanctions compliance in finance

The sanctions regulatory landscape is complex, and compliance places significant demands on financial institutions.

Managing large volumes of false-positives alerts is highly resource-intensive, and genuine matches involving sanctioned individuals or entities require thorough investigation supported by strong internal expertise.

“It is essential for institutions to maintain reliable, well-calibrated sanctions-screening systems that are continuously updated with changes to sanctions lists, and to perform ongoing screening of customers and transactions. Above all, prevision in internal routines and workflows is critical to ensuring robust investigation and sound decision-making. Standardized processes that fail to properly capture and assess alerts create a heightened risk of sanctions breaches,” says Ellen Marie Strømnes

With more than 30 years of experience in the banking sector, Ellen Marie has worked extensively with sanctions regulations. Her operational expertise and deep understanding of the regulatory framework have helped multiple organizations improve both efficiency and accuracy in their sanctions processes.

Contact us to discuss how you can strengthen and streamline your sanctions operations and ensure robust regulatory compliance.

Ellen Marie Holst Strømnes

E-mail: ellen.stromnes@nfrgroup.no

Climate and environmental risks: compliance or competitive advantage?

Climate and environmental risks: compliance or competitive advantage?

Climate and environmental risks are no longer something financial institutions just talk about. It is something supervisors’ price into capital, governance and strategy as the risk has crossed a regulatory threshold.

At the NFR group, we help financial institutions build robust, defensible climate and environmental risk frameworks that prepares for supervisory scrutiny and support sound capital and risk decisions. The focus is on practical implementation: designing and embedding climate risk capabilities that work in real governance, risk and capital processes.

European banking supervision is moving ESG, in particular climate and environmental risk, from a “nice-to-have” sustainability narrative into core prudential risk management.

European banking supervision is moving ESG, in particular climate and environmental risk, from a “nice-to-have” sustainability narrative into core prudential risk management. This shift has been formalised by the EBA through its Guidelines on the management of ESG risks (EBA/GL/2025/01) and its Guidelines on Environmental Scenario Analysis (EBA/GL/2025/04). Together, these frameworks establish minimum standards and reference methodologies for how institutions identify, measure, manage and monitor ESG risks, with a clear supervisory focus on climate and environmental drivers.

Under the EBA framework, compliance is not about producing an ESG report. It is about demonstrating that climate and environmental risk are embedded in governance, risk management and capital and liquidity adequacy processes in a way that is consistent, repeatable and defensible. The ESG risk management guidelines apply from 11 January 2026, with an extended timeline to 11 January 2027 for small and non-complex institutions.

The guidelines explicitly link ESG risk management to prudential governance expectations. Institutions must demonstrate clear ownership and oversight across the three lines of defence, including independent review by internal audit of ESG risk frameworks and governance arrangements. In practice, supervisors expect climate and environmental risk to be treated like any other financial risk driver: governed, controlled, challenged and documented — not merely described.

Our Core Offerings

- Material climate and environmental risk

The identification, assessment and documentation of how physical and transition climate risk affect the business model, balance sheet and risk profile are addressed, including the development of robust materiality assessments that meet supervisory expectations and withstand scrutiny.

- Core risk management frameworks

Climate and environmental risk is integrated into existing prudential structures, including ICAAP, risk appetite frameworks, policies and governance, ensuring they are managed consistently with credit, market, liquidity and operational risks.

- Climate stress testing for capital and strategy

Climate stress testing and scenario analysis are designed to go beyond disclosure, translating climate pathways into quantifiable financial impacts and using the results to inform capital planning, strategic decisions and risk limits.

- Board and senior management accountability

Clear board and executive accountability is established, with climate risk embedded into strategic decision-making, risk oversight and governance in line with supervisory expectation.

- Supervisory readiness and enforcement resilience

Readiness against supervisory expectations is assessed, gaps are identified and prioritised remediation actions are defined, supporting effective supervisory engagement and enabling a transition from expectation-setting to enforceable compliance.

Why NFR?

NFR helps financial institutions build robust, defensible climate and environmental risk frameworks that prepares for supervisory scrutiny and support sound capital and risk decisions. The focus is on practical implementation: designing and embedding climate risk capabilities that work in real governance, risk and capital processes.

With deep experience at the intersection of prudential regulation and banking supervision, NFR understands not only what supervisors expect, but how they assess, challenge and enforce those expectations. This enables the translation of complex regulatory requirements into clear, proportionate and workable solutions tailored to each institution’s size, risk profile and operating model.

NFR’s work is grounded in a structured, methodical approach aligned with supervisory practices and underpinned by a strong understanding of core prudential frameworks, including ICAAP, governance and stress testing. Continuous monitoring of regulatory developments and supervisory priorities ensures institutions stay ahead of evolving expectations.

The result is not just compliance, but confidence: frameworks that institutions are prepared to defend under supervisory review and rely on for capital and strategic decisions.

Does your climate and environmental risk management meet the requirements of the European Banking Authority – or could it become your competitive advantage?

Ingalill Aspholm

Tel. +358 40 084 0314

Are You Ready for EBA’s New Sanctions Requirements?

Are you ready for EBA’s new sanctions requirements?

EBA has published new guidelines that significantly strengthen the requirements for how banks and other financial institutions must implement and follow up on the EU’s restrictive measures and financial sanctions.

In this article, NFR Group highlights the main themes of the guidelines and what they mean in practice for the financial sector. We also provide concrete advice on how banks and other financial institutions can implement sanctions regulations in a structured and risk-based manner within their own organizations.

Are you ready for EBA’s new sanctions requirements?

EBA has published new guidelines that significantly strengthen the requirements for how banks and other financial institutions must implement and follow up on the EU’s restrictive measures and financial sanctions.

In this article, NFR Group highlights the main themes of the guidelines and what they mean in practice for the financial sector. We also provide concrete advice on how banks and other financial institutions can implement sanctions regulations in a structured and risk-based manner within their own organizations.

What are international sanctions?

International sanctions are legally binding or political measures adopted by states, international organizations, or supranational bodies. Their purpose is to uphold principles of international law, promote international peace and security, prevent conflict, and support democracy, the rule of law, and human rights.

Sanctions can be designed in various ways, but within the financial sector, financial and economic sanctions are particularly central. These may include, among other things:

- Asset freeze obligations, which prevent sanctioned individuals and entities from accessing funds and financial assets

- Restrictions on financial transactions and assistance

In addition, there are trade restrictions that limit trade in goods and services, including military equipment, so-called dual-use goods, telecommunications equipment, and luxury goods.

For Norway and Sweden, the implementation of sanctions adopted by the UN Security Council and the EU Council is particularly relevant. In addition, other jurisdictions have their own sanctions regimes with significant global reach, including the United States through the Office of Foreign Assets Control (OFAC) and the United Kingdom through its national sanctions framework.

Sanctions compliance is no longer just a legal issue, but a central part of modern risk management and responsible business governance.

Enforcement of financial sanctions in the EU

In the EU, sanctions regulations are followed up through guidelines issued by the European Banking Authority (EBA) for those parts of the regulatory framework that impose requirements on banks and other financial institutions.

The new EBA guidelines establish common European minimum standards for how financial institutions must design governance arrangements, internal procedures, and control mechanisms to ensure effective compliance with the EU’s restrictive measures/sanctions and national sanctions adopted by Member States.

• EBA Guideline 2024/14: covers governance and compliance requirements for all banks and financial institutions.

• EBA Guideline 2024/15: addresses enhanced requirements for transaction monitoring applicable to all payment service providers and crypto-asset service providers.

Implementation of the EBA guidelines – status in the EU, Sweden, and Norway

EBA GL 2024/14 and 2024/15 apply in the EU from 30 December 2025. It is further expected that the guidelines will be incorporated into the EU anti-money laundering framework, the AML Regulation (EU) 2024/1624, with effect from 10 July 2027.

Sweden: Swedish FSA (Finansinspektionen) has decided to follow the EBA guidelines on restrictive measures from 30 December 2025, in line with other EU countries.

Norway: Norwegian FSA (Finanstilsynet) has not yet confirmed whether GL 2024/14 and 2024/15 will apply in Norway. Norwegian institutions should nevertheless expect increased supervisory expectations regarding governance and controls related to sanctions compliance.

What do EBA’s new guidelines on restrictive measures contain?

EBA’s new guidelines impose extensive requirements on financial institutions’ internal sanctions frameworks, including, among other things:

- Robust, documented internal policies, procedures, and control mechanisms to ensure compliance with restrictive measures

- Comprehensive integration into corporate governance, risk management, and internal control

- Clear definition of roles and responsibilities at all levels of the organization

- Institution-specific risk assessments to identify sanctions risk and the risk of sanctions circumvention

- Effective compliance controls, including monitoring systems, effective screening of customers, beneficial owners, and counterparties against sanctions lists, internal reporting, and documentation

- Transaction monitoring and screening, including analysis of payment patterns to detect and prevent transactions involving listed individuals and entities

- Handling of sanctions hits, asset freezes, and escalation procedures

Taken together, this elevates sanctions of compliance to a more holistic and strategic level within overall corporate governance.

How to ensure effective sanctions compliance in practice

The elements of the EBA guidelines are familiar from the framework applicable to anti-money laundering. We believe that financial institutions will benefit from approaching the EBA’s new sanctions guidelines in the same way they approach AML requirements. Our clear recommendation is therefore to integrate sanctions compliance in line with the model already established for AML processes. This can be achieved through the following eight-step action plan:

- Include sanctions risk in internal policies and institution-specific risk assessments

- Identify which business areas, products, services, and customers are exposed to sanctions and restrictive-measures risk

- Adapt control measures and processes to reduce the risk of breaches or inadvertent circumvention, including screening and transaction monitoring

- Detect and manage exposure, including follow-up of alerts and any asset-freeze obligations

- Document that assessments and controls function effectively in practice

- Clarify sanctions responsibilities and establish escalation procedures to senior management and the board

- Ensure regular employee training to increase awareness and competence

- Establish clear procedures for external reporting to relevant supervisory authorities

A strategic competitive advantage

When implemented correctly, the EBA’s new guidelines deliver not only improved compliance, but also increased operational resilience, reduced regulatory risk, and strengthened trust among customers and authorities. Financial institutions that begin the adaptation process early will be better positioned to meet future requirements – both in the EU and in Norway.

Sanctions compliance is no longer a purely legal issue, but a core element of modern risk management and responsible business conduct.

Our expertise

NFR Group has regulatory experts with a strong knowledge of both anti-money laundering and sanctions regulations. We stay up to date on current requirements and upcoming regulatory changes and have experience and expertise in implementing these requirements efficiently for banks and other financial institutions. Please contact us if you would like to discuss solutions with us.

Need some help to get ready for the EBA's new sanctions requirements?

Ellen Marie Holst Strømnes

Value-creating control functions – structure that drives performance

Value-creating control functions

– structure that drives performance

Control functions form a central part of the financial sector’s ability to create long-term value. By combining independent review with strategic support, control functions such as risk management, compliance, and internal audit contribute both to meeting regulatory requirements and to strengthening the business model and customer trust.

A well-anchored and effective governance of these control functions is therefore crucial to ensure stable and sustainable value creation over time, in a rapidly changing market.

- Methodical and structured

Through clear processes, documented methods, and consistent quality control, control functions ensure that risk assessments and recommendations remain comparable over time. This provides the company with predictability, transparency, and a solid foundation for strategic decision-making.

- Flexible and adaptable

Despite a stable methodology, control functions can quickly adjust their analyses and recommendations as markets evolve, new regulatory requirements emerge, or as the client’s business develops. This adaptability ensures relevance and enables the company to act on up-to-date information.

- Focus on material risks

By prioritizing the risks that have the greatest impact on the business and its customers, such as financial, operational, or technological risks, resources are not spent on less critical issues. This helps the company focus its attention and resources on what truly threatens long-term value.

- Business-aligned

The work of the control function is an integrated part of the company’s business model, processes, and culture. Recommendations and controls are formulated to be practically applicable and to support the organisation’s specific goals, enabling the company to turn advice into tangible improvements.

- Monitoring external developments

By continuously monitoring regulatory changes, technological trends, and industry practices, control functions can provide early guidance and identify new opportunities. This proactive approach strengthens the company’s ability to stay ahead and build competitive advantages.

Why NFR Group?

At NFR Group, we provide control functions that deliver genuine value. With a professional and structured approach, we help companies manage risks, navigate regulations, and strengthen their governance. We offer everything from in-depth analyses to actionable recommendations. Drawing on our experience, we quickly identify the most significant risks and turn complex regulatory requirements into practical, business-focused solutions.

We work with authenticity, transparency, and integrity, building trust throughout every collaboration. Our culture of mutual respect allows us to form long-term partnerships where both client and advisor grow together. This provides a clear advantage through stronger governance, greater confidence, and sustainable value creation in a constantly evolving financial market.

At NFR Group, we strive to be a reliable advisor supporting organizations with responsible solutions tailored for each organization.

Do you want to strengthen your business with control functions that build trust, stability, and long-term value?

A reliable and stronger Internal Audit Function

A reliable and stronger

Internal Audit Function

A well-functioning internal audit function is essential for the financial sector—ensuring transparency, risk awareness, and regulatory compliance at all times. Without proper oversight, your unidentified risks and compliance gaps can undermine long-term stability or your ability to reach the targets.

At NFR Group, we strive to be a reliable partner, providing organizations with actionable, independent, and expert-driven internal audit solutions. With our extensive industry experience we work to continuously enhance your governance framework, strengthen risk management, and compliance with regulatory requirements. Whether you need to establish an internal audit function, reinforce existing capabilities, or conduct specific reviews, our structured and independent approach delivers actionable insights.

Choosing NFR Group means leveraging four key advantages:

- Access to Expertise: Our team consists of top-tier specialists with extensive experience from supervision, the financial sector and internal audit/professional services, ensuring that your organization stays ahead of evolving requirements.

- Cost Efficiency & Scalability: Our flexible solutions allow you to tailor the level of support to your current needs, optimizing costs.

- Focus on Core Business: By outsourcing the internal audit function or getting support for specific reviews, you can direct resources toward core operations and strategic priorities.

- Objective & Unbiased: As an independent provider, we deliver a clear perspective, free from internal influence, helping you uncover blind spots and enhance decision-making with impartial insights.

”An effective internal audit function is not just about risks or compliance — it’s about strengthening the organisations capability to convert business opportunities to long term value. We help organizations turn risk management into a strategic advantage.”

Nicklas Wallenborg, CIA and CCSA, Senior Advisor

With NFR Group as your reliable partner, you gain a strategic, independent, and expert-driven approach to internal audit—ensuring resilience, compliance, and efficiency.

Looking for a reliable provider

of internal audit solutions?

Looking for a reliable provider of internal audit solutions?

Your needs first – Responsible FCP advise, tailored by experts who understand your reality

Your needs first – Responsible FCP advise, tailored by experts who understand your reality

At NFR Group, we bring together expertise from law enforcement, financial supervision, advisory services, and operational roles within the financial sector. With experience from first, second, and third lines of defense in Anti-Money Laundering (AML), and a background spanning AML advisory, fraud prevention, and Financial Crime Prevention (FCP) technology, we help organizations develop tailored solutions that address their unique challenges.

Consistent, achievable, and customized FCP solutions

In many organizations, FCP efforts risk becoming fragmented—particularly when AML processes are developed in isolation from other areas. Balancing regulatory requirements with business needs, customer expectations, and operational efficiencies remains a key challenge. A one-size-fits-all approach rarely works.

We provide advice tailored to each organization’s risk profile, operating model, and regulatory context—ensuring that solutions are both effective and feasible to implement.

Oenables us to support organizations to build coherent, effective and feasible FCP solutions.

NFR Group provides:

- Expertise: We combine specialist knowledge in AML, fraud, and FCP technology with experience from law enforcement, financial supervision, advisory services, and operational roles in the financial sector.

- Client-centric solutions: Our expertise enables us to support organizations with solutions adapted to their unique situation, ensuring effective and feasible solutions.

- Holistic approach: Our understanding of FCP in the broader risk context enables us to provide advice that considers the full picture.

- Risk-Based and practical: Our advice is grounded in operational realities and focused on achieving compliance in a way that supports and efficiency.

“Our role is to support organizations in finding the most suitable solution for their organization by ensuring compliance and efficient processes, while minimizing effects on customer experience. In this way organizations can start fighting financial crime and not only put focus on compliance.”

Angelica Dymne, Advisor, NFR Group

At NFR Group, we strive to be a reliable advisor supporting organizations with responsible solutions tailored for each organization.

Looking for trusted FCP advice

tailored to your risk landscape?

Looking for trusted FCP advice tailored to your risk landscape?